Health Insurance Coverage Isn’t Always What It Seems

Many people believe that buying a high-value health insurance policy guarantees full financial protection. A ₹10 lakh or ₹20 lakh cover sounds reassuring, but what many policyholders don’t realize is that hidden clauses buried in fine print can drastically reduce claim amounts when a medical emergency strikes.

Insurance policies are structured with technical terms, exclusions, sub-limits, and clauses that aren’t always made clear during the purchasing process. This can result in unexpected out-of-pocket expenses, turning what should have been a safety net into a frustrating financial burden.

A policyholder might assume that their policy covers hospitalization in full, but when they file a claim, they discover:

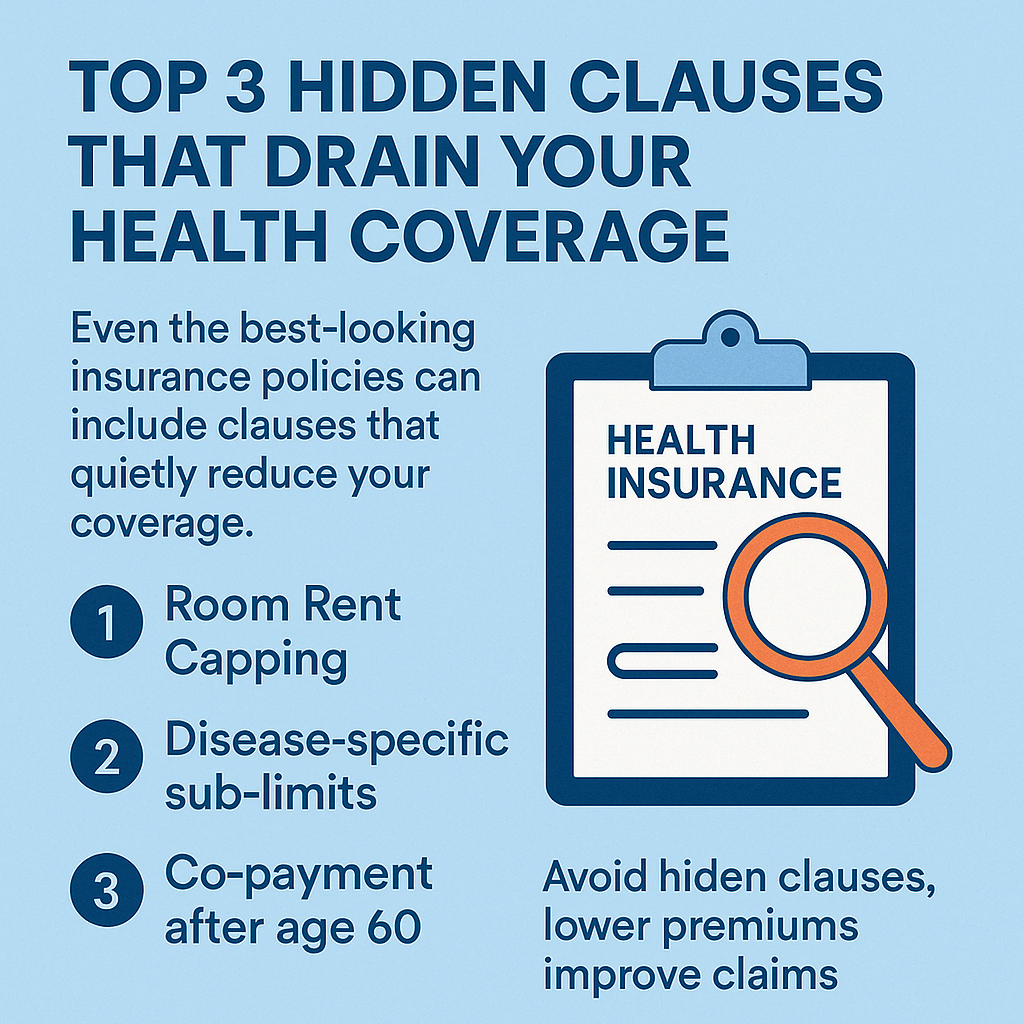

- Room rent capping limits reimbursement, affecting all associated costs

- Disease-specific sub-limits restrict coverage for treatments like heart surgery or dialysis

- Co-payment clauses force policyholders to pay a portion of the bill themselves

These limitations aren’t immediately obvious until a claim is denied or significantly reduced, leaving patients and families scrambling for money despite having insurance.

The Hidden Clauses That Drain Your Benefits

Many policyholders only realize these restrictions when it’s too late—after hospitalization, during claim settlement. Let’s break down some of the most common hidden clauses that can result in heavy out-of-pocket expenses.

1. Room Rent Capping

One of the biggest surprises in health insurance policies is room rent limit restrictions. Here’s how they work:

- Insurance policies cap the maximum daily room rent cost they will cover.

- If a policy limits room rent to ₹5,000 per day, but the insured selects a ₹8,000 per day room, they don’t just pay the difference.

- Instead, all associated medical charges—doctor fees, surgery costs, ICU charges—are proportionately reduced, leading to massive personal expenses.

Case Study: A Costly Miscalculation

A 38-year-old patient in Delhi had a ₹10 lakh health insurance policy, assuming it would cover all hospitalization costs. However, his policy had a ₹5,000 per day room rent cap, but he stayed in a ₹7,000 per day room.

Here’s what happened:

- Surgeon Fees: Claimed ₹1,00,000, approved ₹71,000

- ICU Charges: Claimed ₹25,000, approved ₹17,850

- Diagnostic Tests: Claimed ₹15,000, approved ₹10,710

- Total Out-of-Pocket Expenses: ₹58,000

Despite having a ₹10 lakh policy, the patient paid ₹58,000 from his savings—all because of room rent capping.

2. Disease-Specific Sub-Limits

Some policies impose restrictions on certain illnesses or treatments, regardless of the total sum insured.

Examples include:

- Heart Disease Coverage: Policy covers ₹5 lakh, but imposes a ₹2 lakh limit for cardiac surgery.

- Kidney Dialysis: The overall sum insured is ₹10 lakh, but dialysis has a ₹50,000 cap per year.

- Cataract Surgery: The total sum insured is ₹5 lakh, but cataract treatment is capped at ₹30,000 per eye.

These sub-limits drastically reduce reimbursements, forcing patients to cover significant costs from their own pockets.

3. Co-Payment Clauses for Senior Citizens

Many policies for senior citizens include co-payment clauses, requiring policyholders to pay 10-50% of medical expenses themselves.

For example:

- A senior citizen with a ₹5 lakh policy undergoes surgery costing ₹4 lakh.

- If their policy has a 20% co-payment clause, they must pay ₹80,000 from their savings.

This clause can go unnoticed until hospitalization occurs, leaving older patients with unexpected financial stress.

How AI-Driven Tools Help Identify Hidden Clauses

The best way to avoid these costly surprises is to identify restrictive clauses before purchasing a policy. AI-powered insurance comparison tools analyze policy documents, highlight exclusions, and flag problematic clauses upfront, making the selection process easier and more transparent.

How AI Helps in Choosing the Right Health Insurance

- Scans Fine Print for Hidden Clauses

AI tools review policy documents and detect restrictions like:

- Room rent capping

- Sub-limits for specific diseases

- Co-payment requirements

- Waiting periods for pre-existing conditions

- Provides Real-Time Comparisons Across Multiple Insurers

- AI compares plans side-by-side, highlighting pros and cons.

- Users can quickly see which policy offers full coverage versus one with hidden deductions.

- Flags High Claim Rejection Rates

- AI analyzes historical claim settlement ratios of insurers.

- Helps users avoid companies with poor claim approval records.

- Simplifies Complex Terms with Clear Explanations

- Breaks down difficult insurance jargon into easy-to-understand insights.

- Ensures policyholders understand exclusions before buying.

Example: AI in Action

A 45-year-old policyholder wanted to buy a ₹10 lakh policy. They used an AI-driven insurance comparison tool, which revealed:

- Policy A had a ₹5,000 room rent cap and 10% co-payment on hospitalization.

- Policy B had NO room rent cap, NO co-payment, and covered all hospitalization costs fully.

Though Policy A looked cheaper, it had several hidden limitations. The AI analysis helped the policyholder choose Policy B, ensuring maximum financial protection.

Final Thoughts: Make Informed Choices & Avoid Unpleasant Surprises

Health insurance is meant to reduce financial stress during medical emergencies, but hidden clauses can drain your coverage unexpectedly. Choosing the right policy requires careful analysis to identify room rent caps, disease-specific sub-limits, and co-payment clauses before purchasing.

The best way to avoid these pitfalls is to leverage AI-powered tools that analyze policies and flag restrictions upfront. With AI-driven insights, policyholders can make data-backed decisions, ensuring they get the coverage they need without hidden surprises.